Stacey Isaac Berahzer is a Senior Project Director for the Environmental Finance Center at the University of North Carolina, and works from a satellite office in Georgia.

Water rate increases can get even more controversial when there is the perception that the related increase in revenue is going to fund government activities other than water service.

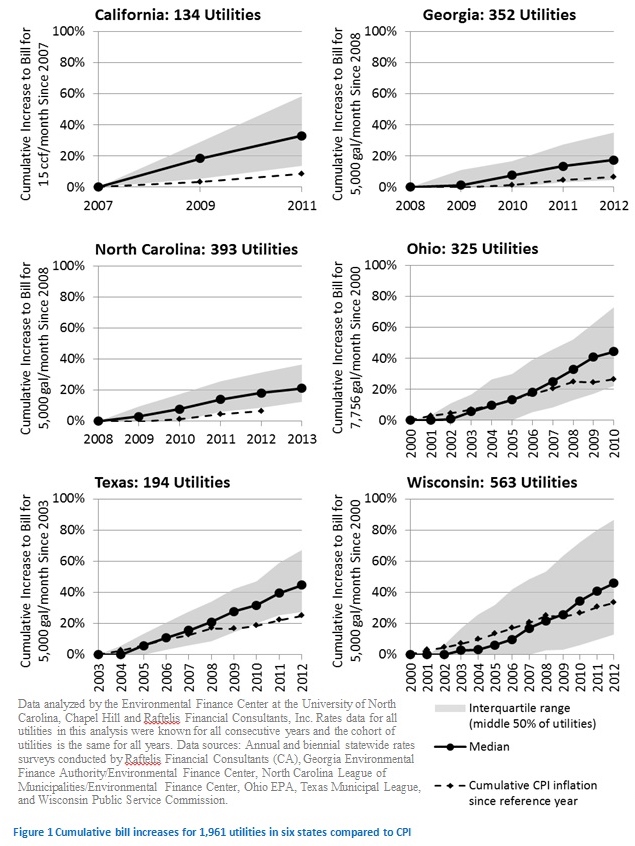

With the economic downturn, local governments are having a harder time balancing their budgets and the temptation to draw from utility funds becomes harder to resist. Stories are popping up in the press, such as objections over a 59% (utility) rate increase over a 13-year period, in order to hold millage rates steady in one local government. Several factors play into whether this is an unusually high rate of increase. Inflation is one important factor. In the last ten years, the Consumer Price Index (CPI) measure of inflation rose by more than 25%. The power of compounding involved with annual rate increases over the 13 years is also an important consideration. But, if we compared this increase to, say about 2,000 utilities from six states across the country, would the 59% be an outlier?

For the states of Ohio and Wisconsin, where the data in the chart below goes back 13 years, this 59% actually falls within the grey-shaded interquartile range, or middle 50% of utilities.

Figure 1 Cumulative bill increases for 1,961 utilities in six states compared to CPI

But, even if the degree of rate increase is on par with other water utilities, are the revenues generated from the higher rates being inappropriately used to bail out other sectors of the local government?

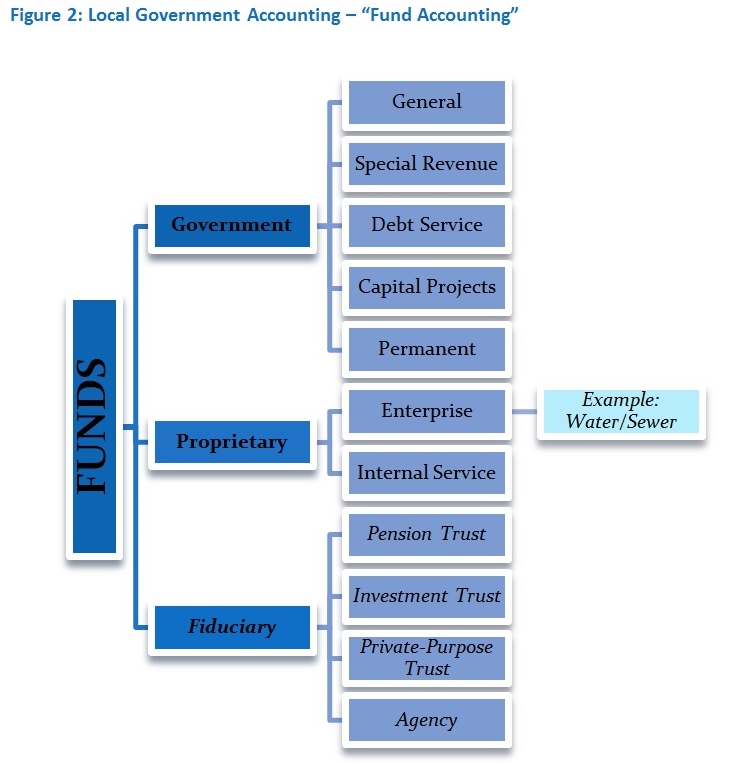

Fund Accounting 101

Local government accounting involves maintaining a series of “funds” for explicit purposes. The diagram below depicts the types of funds. The two that are most relevant here are the general and enterprise funds.

The idea is for utility enterprise funds to be independent of the parent city or county government.

As the name suggests, the “general fund” is basically the default fund. It is used to account for general operations and activities that do not require the use of other funds. The general fund is chiefly comprised of property and sales tax revenue paid to the local government.

A special type of proprietary fund, the “enterprise fund,” is used for services provided to the public on a user charge basis, similar to the operation of a commercial enterprise. Water and wastewater utilities are common examples of government enterprises.

Normal and repeated transfers in/out of an enterprise fund are not recommended practice. A local government that needs to consistently subsidize its utility by transfers from the general fund to the enterprise fund is missing the mark of fund distinction/independence. Significant transfers to the general fund may also raise questions of equity. If the citizens of a city, for example, are paying more in property taxes in order to subsidize a water utility, while water utility customers outside the city limit are not contributing to the utility via taxes, this may represent an inequitable scenario.

In Practice, Lines are harder to Draw

In reality, the majority of local governments have some interplay among these different funds, some more easily justified than others.

The Spectrum of Fund Interactions

1. Fund Transfer – In its least defensible form, this would involve a transfer, almost, if not every year from the utility fund to the general fund. To be really hard to justify, the transfer would be large, relative to the overall budget of the water utility, and the amount would change from year to year, just depending on the amount of shortfall in the general fund for a given year.

2. Return on Investment – In this case, a water utility provides a payment to the parent government due to some, almost philosophical, understanding that the local government ultimately is the entity that incurs the “risk” involved in large debt etc. on behalf of the utility.

3. Franchise Fee – Typically, franchise agreements establish the terms under which a utility may use the municipal right of way. This rental fee is often a specified percentage of the utility’s gross receipts within the municipality but can be determined based on other factors. While more common for external entities such as private cable service providers, franchise fees are paid by some government water utilities to their parent local governments.

4. Payment in Lieu of Taxes – This is where money is transferred from the water utility to the general fund under the principle that the local government would have received a related amount in taxes had the utility property been owned by a private, taxed entity.

5. Cost Allocation – As far as money moving from an enterprise fund to the general fund goes, this one can actually be considered a best practice. Here, there is a method for determining the proportion of a centrally provided service, such as information technology, human resources, accounting and facility maintenance that is attributed to the utility. Ideally, these services are initially paid through the general fund, or an internal service fund, and charged back to the departments and programs that directly benefited from them. The process should begin with an allocation plan that outlines the protocol. The plan can include specifics such as square footage as an appropriate factor to allocate janitorial costs. In terms of local government personnel, it is certain that some local government officials, not directly employed at the water utility, spend a portion of their time on utility issues. Determining how much, for instance, of a County Manager’s time is spent on the water/sewer system and allocating a percentage of his/her salary from the water/sewer budget is a different matter than a simple “fund transfer.” Local governments are encouraged to try to determine this percentage and allocate it as such. For a simple example, the County Manager may keep a log of the number of phone calls he/she is involved in that relate to the water/sewer fund. If, on average, two out of 10 calls for the day relate to water and sewer issues, then this helps make the case for 20% of the manager’s salary to come from the water/sewer utility budget. The goal would be to employ a defensible process for allocating the percentage of time.

How credit rating agencies view these movements of money is worth mentioning. According to Standard & Poor’s, what is most important in a transfer from a public enterprise fund to the general fund of the governing body is that the transfer is “well-researched, flexible, consistent, and well-communicated.” How a utility reacts, or better yet, anticipates its operating environment largely factors into a utility’s rating.

Conclusion

There may be a myriad of unfortunate cases where the water utility is seen as the “cash cow” that a poorly-run local government can rely on to prop-up its general budget. In the end, the utility owes it to itself (and its customers) to employ at least some of these avenues to tease out the cost of its own core business from the, usually, undeniable benefits it enjoys from its relationship with the parent government. Water rate increases may become easier to explain, if not more palatable.

Water rate increases get controversial when people think the revenue is going to fund other government activities: http://t.co/4YIIUZWPI5

— Envr. Finance Center (@EFCatUNC) September 27, 2013

Nice and informative article. Thanks for sharing the information with us. Learned a lot of things.

While cost allocation may be considered a best practice, in reality it is the dollar tranfer most prone to abuse and least pubically acknowledged. You need look no further than North Carolina to see city managers loading up their charges to their enterprise funds for services rendered in order to work around the 3% suggested cap the state government has imposed on PILOTs. It is not uncommon to see 80% – 97% of finance directors, city managers and other general fund departments’ time charged back to enterprise funds.