Shadi Eskaf is a Senior Project Director for the Environmental Finance Center at the University of North Carolina, Chapel Hill.

Our research shows that water rates have been rising faster than CPI inflation in the past few years for hundreds of utilities, particularly after the financial crisis. In some states, however, there were also many utilities whose rates failed to keep pace with inflation.

From a rate-setting perspective, utilities that raised rates more frequently had a double advantage over utilities that raised rates only occasionally or rarely. First: the average annual rate increase was lower than the one-time rate increases of utilities that occasionally raised rates, reducing the rate shock that customers experienced when rates rose. Second: despite the lower average rate increases, utilities that raised rates more frequently accumulated, on average, a larger total increase in rates in a five-year period than utilities that raised rates only occasionally.

Trends of Rate Increases

Rate changes are crucial for a utility’s financial health in order to keep revenues consistent with changing (usually rising) costs and to compensate for long-term trends of declining water use. A previous blog post reported that operating expenses were growing faster than operating revenues for many utilities, especially between 2008 and 2010. Infrastructure capital needs and costs are also on the rise. Since water utilities obtain most of their revenues from customer charges, it is often necessary to adjust rates to ensure financial sustainability.

The nationwide trend of rising water rates has been noticed and reported on recently by national news sites, prominent online water news networks, blogs, and academic studies. These reports invariably provide statistics on the percent increases of water rates over time, either for specific utilities or aggregated statistics for a small sample of utilities across the country. Because it is difficult to obtain historic water rates data, the sample sizes tend to be small (30-100 is typical) and focused mostly on large utilities.

Expanding on these efforts, as part of the research for Water Research Foundation project #4366, the EFC at UNC compiled and analyzed historic water or combined water and wastewater rates for 1,961 local government utilities in six states, including many small and large water systems. The data were obtained from annual or biennial statewide rates surveys in California, Georgia, North Carolina, Ohio and Texas, and directly from the Wisconsin Public Service Commission that regulates the rates government-owned utilities in the State of Wisconsin charge their customers.

How Much are Rates Rising?

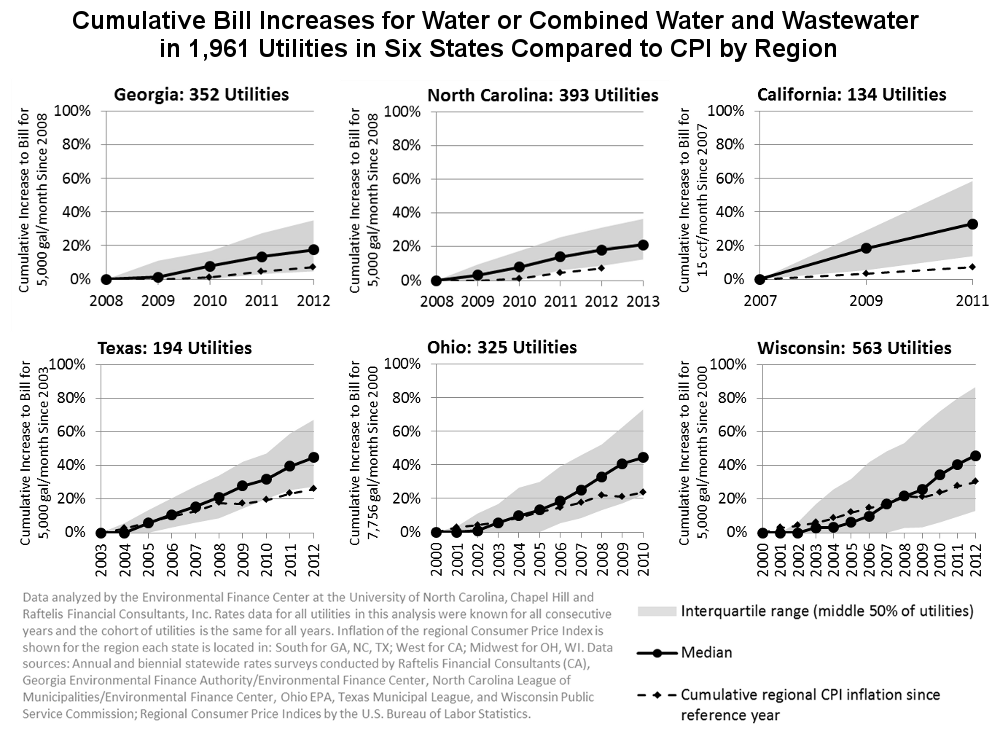

The figure below, which you can click to enlarge, shows how the monthly water or monthly water and wastewater bill for a specific consumption point rose each year for the same cohort of 1,961 utilities in six states. The graphs also include the cumulative Consumer Price Index inflation in the corresponding region for comparison. Rates for the majority of utilities rose faster than inflation in the past few years, although there are significant variations across utilities between and within states. For example, by 2012, half of 194 local government utilities in Texas had a monthly total bill for 5,000 gallons that, in nominal terms, was at least 45% higher than in 2003. The middle half of these utilities had bills that were 27% to 67% higher in 2012 than in 2003, showing considerable variability in rate increases within the state alone. In those ten years, the Consumer Price Index for the South region rose by a total of 26%, indicating that more than three-quarters of the 194 Texas utilities raised water and/or combined rates between 2003-2012 faster than inflation and the rise of other consumer goods.

Though the exact size of the cumulative rate increases varied from state to state, water/combined rates rose faster than inflation in all six states. Prior to 2007, the median rate increase in Ohio and Texas was on par with inflation, and was in fact below inflation in Wisconsin. After 2007, CPI stagnated in all regions during the recession (resulting in deflation in one year), but water/combined rates continued to rise at a steady rate, resulting in more utilities raising rates faster than cumulative inflation in their region during that time period in all three states. In North Carolina, Georgia, and California, the majority of utilities also raised rates faster than regional CPI inflation since 2007 or 2008.

There were, nonetheless, many utilities whose rate increases did not keep pace with inflation, particularly prior to 2007. It is possible that these utilities were in a financial position that did not require them to generate additional revenue.

Cumulative Bill Increases for Water or Combined Water and Wastewater in 1,961 Utilities in Six States Compared to CPI by Region – click to enlarge

Although CPI inflation has very little or almost nothing to do with rising utility costs or capital needs, it is useful to consider these results from the point of view of the consumer. What this all means is that at a time when incomes were/are stagnating or declining on average, and consumer products’ prices also leveled off for a few short years, the price for water rose at a more substantial rate in most communities. This likely created more affordability issues for utilities in recent years than in the past (read here about addressing customer affordability).

How are Utilities Raising Rates?

From the utilities’ perspective, rising costs and declining water use necessitates rate increases. There are generally two ways to go about this: raise rates a little at a time frequently, or hold off on rate increases for a couple or few years and then have a significant rate increase all at once. There are, of course, other ways to go about rate increases, including linking rates to cost indices like CPI, but most utilities have rate increases in those two ways. Our research shows that, from the perspective of the utility and possibly the customer, utilities that chose to raise rates frequently performed better than utilities that chose to avoid rate increases for a few years.

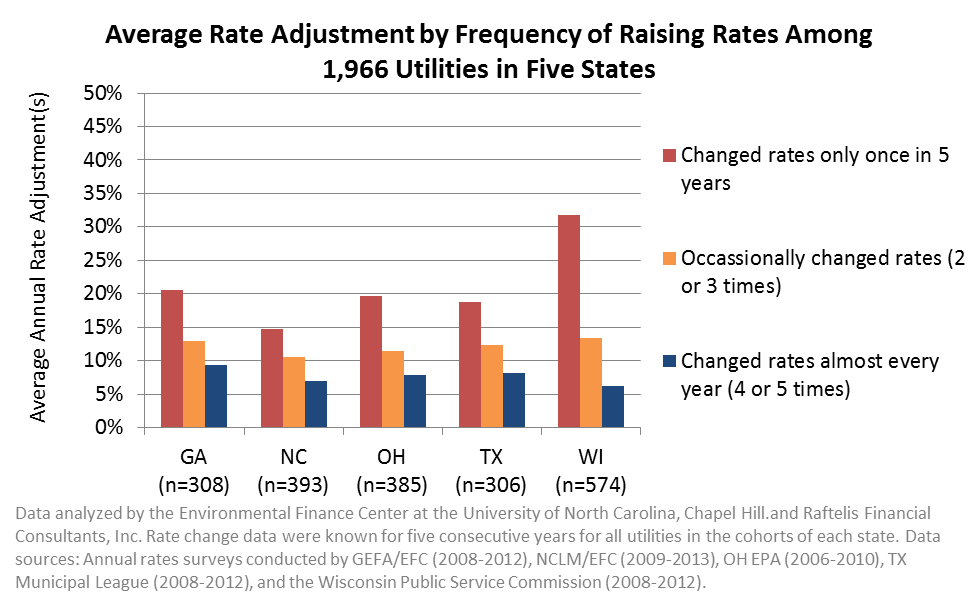

Firstly, utilities that increased rates less frequently tended to have larger rate increases than utilities that increased rates more frequently. This trend is illustrated in the next graph. The average one-time rate adjustments are (sometimes drastically) higher for utilities that changed rates only once in five years compared to utilities that changed rates almost every year. In Ohio, for example, utilities that increased their rates only once in the five year period averaged a 19% rate increase, compared to an average increase of 7%/year for Ohio utilities that raised rates almost every year in the same time period. Lower rate increases are easier for customers to adjust to. No one wants to see their water bill go up by 30% or more in one year, even if rates had not been raised for several years.

Average Rate Adjustment by Frequency of Raising Rates Among 1,966 Utilities in Five States – click to enlarge

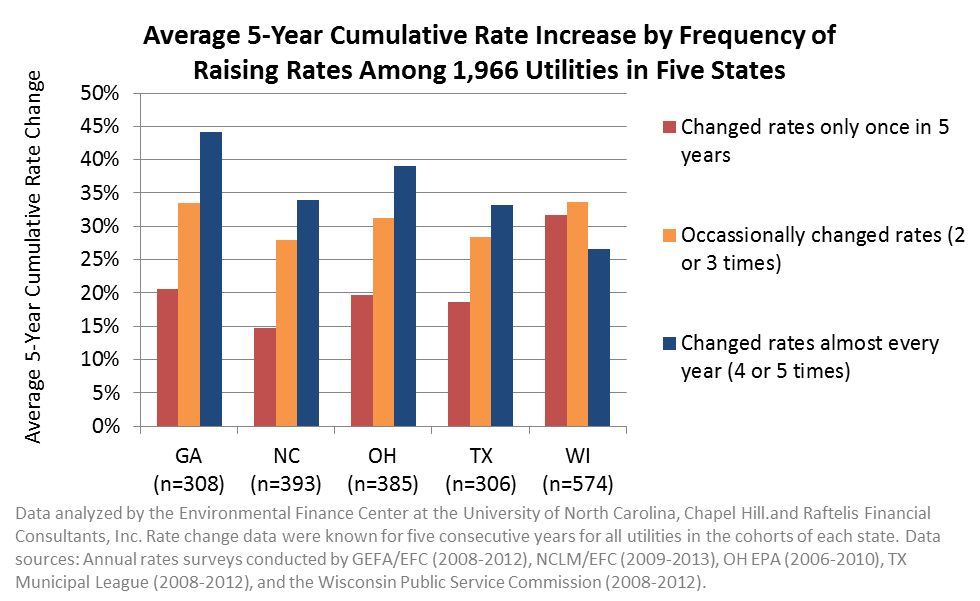

Secondly, utilities that raised rates frequently had generally, in the long-run, accumulated a larger total increase in rates than utilities that raised rates infrequently, despite raising rates only by smaller percentages each year. This is shown in the next graph. The cumulative effect of more frequent, smaller rate increases generally outsized the larger, one-time rate increases. For example, although the utilities in Georgia that raised rates almost every year only raised rates by an average of about 9% per year, the cumulative rate increases amounted to an average of 44% after five years. By comparison, the Georgia utilities that raised rates only once in five years had a rate increase of 20%.

Average 5-Year Cumulative Rate Increase by Frequency of Raising Rates Among 1,966 Utilities in Five States – click to enlarge

From a utility’s perspective, it seems that there are long-term financial and short-term customer service benefits to raising rates frequently: the annual rate increases can be small in size, avoiding customer rate shock, while enabling the utilities to accumulate greater rate increases over time than if the utility maintains the same rates for several years and requires a very large one-time rate increase. Is this what most utilities opted to do in these five states? Not quite. Only 25%-42% of utilities in each state adjusted their rates almost every single year in Georgia, North Carolina, Ohio and Texas, compared to 17%-36% of utilities that did not adjust rates or adjusted rates only once in those five years. Rate adjustments were much less frequent in Wisconsin where the Public Service Commission regulates rate increases for government-owned utilities.

Frequency of Rate Adjustments in Five Consecutive Years Among 1,966 Utilities in Five States – click to enlarge

Whether a utility increases rates annually or only once every five years, ultimately rate adjustments should reflect changes to utility operating and capital expenses, while being mindful of customer affordability problems. Although this blog post focused on rate increases, reducing costs should also be a high priority for utilities (but not at the expense of delaying necessary expenses which could then lead, in the long-run, to poor service and may harm public health). There are many ways to reduce energy costs, non-revenue water, and even operating and capital costs through partnerships with other utilities.

More on rates, revenues and financial strategies is and will be posted on this blog, and a comprehensive report will soon be published by the Water Research Foundation. Special thanks to my colleagues at the Environmental Finance Center at UNC: Jeff Hughes, Mary Tiger, Sarah Royster and Dayne Batten.

My brother suggested I may like this web site.

He used to be entirely right. This post truly made my day.

You cann’t believe simply how much time I had spent for this info!

Thanks!