Mary Tiger is the Chief Operating Officer of the Environmental Finance Center at the University of North Carolina.

A few months ago a group of over 20 utility managers from some of the largest water utilities in the country convened in Denver, Colorado to discuss strategies that are working (and not working) to mitigate and master issues facing their individual utilities. Beyond having size in common, it was a diverse group, representing a spectrum of ownership and service models, as well as geographical and service characteristics. As such, the impact of common trends in the industry (as projected in the Water Research Foundation report “Forecasting the Future: Progress, Change, and Predictions for the Water Sector”) varied greatly between them.

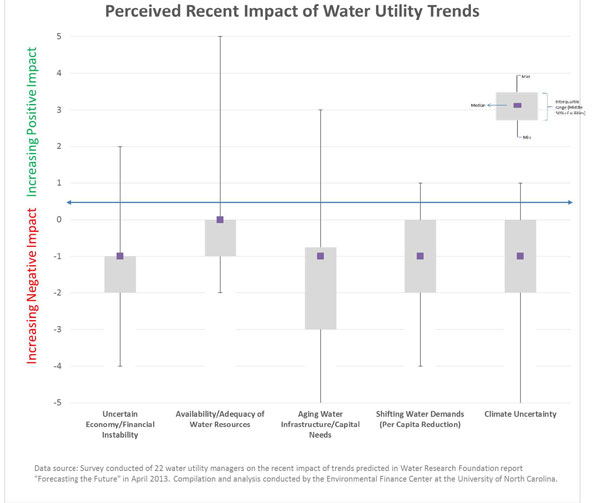

The graph below shows the assessed impact of five of the ten common trends among the group of water utility leaders that have had the most negative impact in the past five years: uncertain economy/financial instability, availability/adequacy of water resources, aging water infrastructure/capital needs, shifting water demands, and climate uncertainty[1]. Some trends have been positive for some utilities while quite detrimental for others (such as the availability/adequacy of water resources). Although these extremes are largely a product of system characteristics and geographic differences, human nature (or at the very least the nature of human leaders) seeks strategies to mitigate and master the challenges dealt in an effort to turn a negative trend positive.

Survey results on the recent impact of prevalent trends in the water utility industry

The Environmental Finance Center facilitated a discussion between the water utility mangers on strategies used and needed to address these trends. Many ideas were discussed, but the following strategies were common in addressing risks associated with all of these five major industry trends. And while none are ground-breaking in their revelation, they each require the sometimes difficult (yet potentially positive) task of coordination and collaboration.

Communication

Communication strategies have helped utilities secure the rates necessary to ensure financial stability and address capital needs through understanding. The group stressed a need to connect infrastructure needs to public health, environmental protection, and economic development and the rates that customers pay. (In many ways, pricing is a sub-category of communication; it wouldn’t be an EFC blog post without mentioning that.)

Partnership

Whether for watershed planning to meet water availability and adequacy challenges, system interconnections, or conservation programming, utilities can create system redundancy and financial diversification through partnerships. Water utilities are partnering with other departments, other utilities, state agencies, and even, insurance companies cushion the uncertain risk associated with prevalent trends.

Planning

Arriving at some sort of agreed upon prediction (or ideally range of predictions), although admittedly a never -accurate prediction, helps to activate other relevant strategies, such as communication and partnership. A water resource plan, climate adaptation plan, capital improvement plan, or financial plan serves as a platform from which management and financial decisions (as well as many other decisions) can be made. In fact, plans are like pie; they’re best when shared.

Within each of these broad strategies are plenty of different and even diverging approaches. As such, they remain focus for the water industry to mitigate and master an uncertain future. You can read more about this topic in the forthcoming Water Research Foundation report on “Steering Innovation in Water Utility Finance and Management.”

[1] The other five trends projected in “Forecasting the Future” were increasing/expanding regulations, changing workforce, efficiency drivers/resource optimization, mass/social media explosion, and expanding technology application.

Leave a Reply