Shadi Eskaf is a Senior Project Director for the Environmental Finance Center at the University of North Carolina, Chapel Hill.

Ratio of Operating Revenues to Operating Expenses for 62 Utilities Nationwide

A couple of months ago, we blogged that water utilities’ operating revenues are generally continuing to grow every year, but that there was a slowdown of revenue increases in recent years, particularly after 2008. At the same time, expenses are also rising. Does this mean that expenses have caught up to revenues and that the majority of utilities are now experiencing revenue shortfalls?

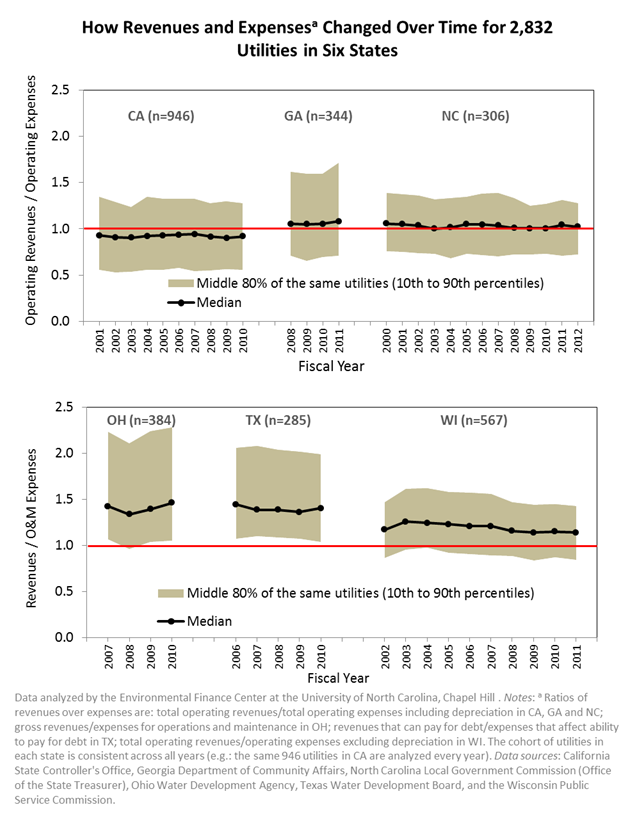

As part of the research for Water Research Foundation project #4366, we (the Environmental Finance Center at UNC and Raftelis Financial Consultants, Inc.) collected and analyzed financial data for local government water and wastewater utilities from state agencies in California, Georgia, North Carolina, Ohio, Texas and Wisconsin. Comparing the ratio of operating revenues to operating expenses (sometimes called operating ratio) over time for 2,832 water and combined utilities in those six states reveals whether the gap between annual revenues and expenses was narrowing for the majority of local government-owned utilities in recent years. The figure below, which you can click to enlarge, tracks the median and range of the ratios for the cohorts of utilities in each state in every year shown. For example, the same 946 utilities in California were analyzed in every fiscal year between 2001 and 2010. The definition of operating expenses varied slightly between the states, depending on data availability, and is explained in the footnote of the graph. The main difference is that depreciation is included in operating expenses for California, Georgia and North Carolina, but not for any of the other states. While depreciation is not an expenditure that a utility makes, it can be viewed as a surrogate for the minimum annual capital expense required to maintain infrastructure at the current service level.

How Operating Revenues and Expenses Changed Over Time for 2,832 Utilities in Six States

The figure shows good news and not-so-good news for water utilities. The good news is that throughout the analyzed years, more than half of the utilities in all states except California had operating revenues that exceeded operating expenses, with or without depreciation. In fact, fewer than 10% of utilities in Ohio and Texas in any year of analysis had lower operating revenues than operating expenses excluding depreciation. Utilities operating in these conditions would have to use their reserves, transfers and/or non-operating revenues to fill the gap between day-to-day operations and maintenance expenditures and their operating revenues, leaving little to no revenue to cover capital expenses. Nevertheless, the majority of utilities in five of the six states collected more in operating revenues than their operating expenses in recent years. It would therefore be inaccurate to claim that “revenues are falling short of expenses” when discussing utilities collectively across the states.

However, the not-so-good news is that the trends indicate that more utilities in several states across the country experienced greater financial difficulties around FY2008–FY2010. There is not enough data from these data sets to comment on trends since FY2010. Between FY2008 and FY2010, the ratios either declined or were low in all six states. Nonetheless, the financial performance of utilities in those years was not significantly worse than in prior years. In California, North Carolina and Wisconsin – the three states with longer time series of data – the financial performance of utilities in FY2008-FY2010 was similar to the financial performance of the same utilities in FY2002–FY2004. Thus, although utilities in geographically disperse areas and under different governance structures across the country experienced lower operating ratios and additional strains on finances towards the end of the decade, these difficulties were similar to those experienced in the beginning of the decade. Essentially it means that the gains made in mid-decade were eliminated and utilities returned to lower levels of financial condition. For many utilities, going through two periods of financial difficulties within ten years can pose significant challenges to their long-term financial stability.

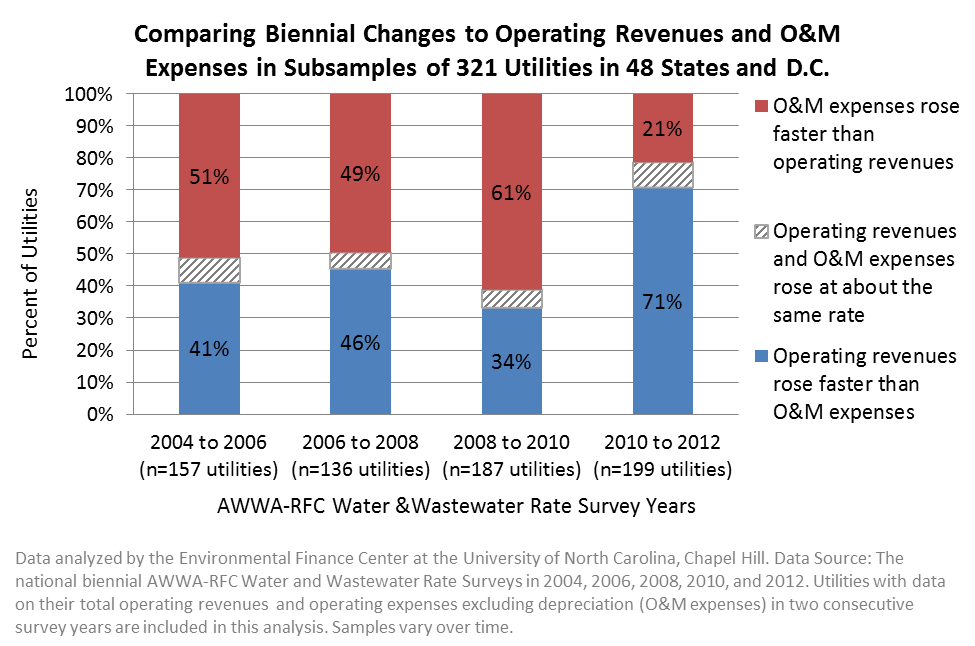

Widening the analysis to include hundreds of utilities across 48 states and in Washington D.C. using data from the biennial AWWA-RFC Water & Wastewater Rate Surveys show that the gap between operating revenues and expenses for operations and maintenance (operating expenses excluding depreciation) was narrowing for most utilities for several years in the past decade, but that a recovery may be occurring since 2010 as shown in the graph below. Every two years prior to the 2010 survey year, more than half of the utilities experienced faster growth in O&M expenses than they did in operating revenues, negatively affecting the utilities’ ability to save and pay for debt and capital costs and remain financially self-sufficient. Since the 2010 survey year, operating revenues increased faster than O&M expenses for 71% of 199 utilities. More time and data are needed to verify whether this reverse in trend is a sign of improving conditions for utilities nationwide or whether it was an anomaly.

Comparing Biennial Changes to Operating Revenues and O&M Expenses in Sub-samples of 321 Utilities in 48 States and D.C.

At the local level, utility managers, board members and customers will be more concerned with how the operating ratio for their own utility is trending. Even if the majority of utilities in the state have improving ratios over time, some utilities may be trending downwards or may have greater expenses than revenues. It is essential for utilities to track their own financial performance ratios and indicators over time and set targets in policies to monitor and ensure financial stability regardless of changing operating conditions.

The dramatic change in biennial changes to operating revenues and O&M expenses could use some anecdotal examples (a few phone calls should do the trick). The utilities I work with raised rates as a result of their experience during 2008-2010 and simultaneously reduced labor cost growth through white collar freezes. What has happened to demand has varied – wealthier, growing communities have seen demand rebound while others are seeing a continuation of demand declines.

That is a great point, Myron. In fact, in the report we are writing, we take the analysis in the direction you suggested. We analyze the operating ratios for hundreds of utilities in each state (in the 2008-2010 period) and how each utility raised its rates in the subsequent year. We’ve found that there are a handful of utilities that had low ratios in one year and had double-digit rate increases immediately afterwards. But we’ve also found that the magnitude of rate increases varied so much that there wasn’t a very clear link (at the state level) between operating ratio in one year and rate increases in the next. Perhaps we can solicit some nice anecdotal examples from individual utilities in response to our blog discussion here (hint, hint), especially to understand how utilities were able to lower costs as well.

We expect to post some of our analysis on trends in rates on this blog soon.